Several links below. A few excerpts below as well. @Willence How is the mortgage community reacting to this?

A little-noticed revamp of federal rules on mortgage fees will offer discounted rates for home buyers with riskier credit backgrounds — and force higher-credit homebuyers to foot the bill

Fannie Mae and Freddie Mac will enact changes to fees known as loan-level price adjustments (LLPAs) on May 1 that will affect mortgages originating at private banks nationwide

The result, according to industry pros: pricier monthly mortgage payments for most homebuyers — an ugly surprise for those who worked for years to build their credit, only to face higher costs than they expected as part of a housing affordability push by the US Federal Housing Finance Agency.

“It’s going to be a challenge trying to explain to somebody that says, ‘I worked my whole life for high credit and I’ve put a lot of money down and you’re telling me that’s a negative now?’ That’s a hard conversation to have.”

“It’s unprecedented,” added David Stevens, who served as Federal Housing Administration commissioner during the Obama administration. “My email is full from mortgage companies and CEOs [telling] me how unbelievably shocked they are by this move.”

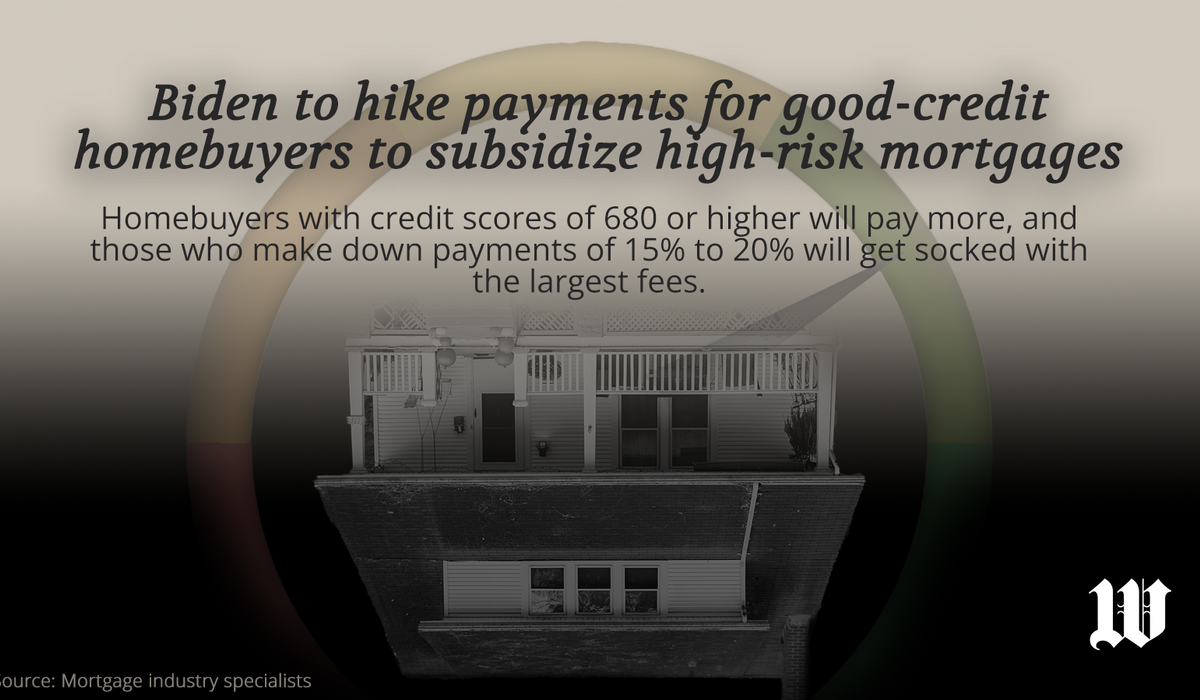

Under the new rules, high-credit buyers with scores ranging from 680 to above 780 will see a spike in their mortgage costs – with applicants who place 15% to 20% down payment experiencing the biggest increase in fees.

“This was a blatant and significant cut of fees for their highest-risk borrowers and a clear increase in much better credit quality buyers – which just clarified to the world that this move was a pretty significant cross-subsidy pricing change,” added Stevens, who is also the former CEO of the Mortgage Bankers Association.

nypost.com

nypost.com

www.washingtontimes.com

www.washingtontimes.com

A little-noticed revamp of federal rules on mortgage fees will offer discounted rates for home buyers with riskier credit backgrounds — and force higher-credit homebuyers to foot the bill

Fannie Mae and Freddie Mac will enact changes to fees known as loan-level price adjustments (LLPAs) on May 1 that will affect mortgages originating at private banks nationwide

The result, according to industry pros: pricier monthly mortgage payments for most homebuyers — an ugly surprise for those who worked for years to build their credit, only to face higher costs than they expected as part of a housing affordability push by the US Federal Housing Finance Agency.

“It’s going to be a challenge trying to explain to somebody that says, ‘I worked my whole life for high credit and I’ve put a lot of money down and you’re telling me that’s a negative now?’ That’s a hard conversation to have.”

“It’s unprecedented,” added David Stevens, who served as Federal Housing Administration commissioner during the Obama administration. “My email is full from mortgage companies and CEOs [telling] me how unbelievably shocked they are by this move.”

Under the new rules, high-credit buyers with scores ranging from 680 to above 780 will see a spike in their mortgage costs – with applicants who place 15% to 20% down payment experiencing the biggest increase in fees.

“This was a blatant and significant cut of fees for their highest-risk borrowers and a clear increase in much better credit quality buyers – which just clarified to the world that this move was a pretty significant cross-subsidy pricing change,” added Stevens, who is also the former CEO of the Mortgage Bankers Association.

How the US is subsidizing high-risk homebuyers — at the cost of those with good credit

Experts say an “unprecedented” overhaul of mortgage fees would result in higher payments for most buyers.

Biden to hike payments for good-credit homebuyers to subsidize high-risk mortgages

Homebuyers with good credit scores will soon encounter a costly surprise: a new federal rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.

www.washingtontimes.com